Global Power Battery Market: Chinese Dominance Intensifies in H1 2025

Recent data from South Korean market research firm SNE Research reveals that the global installed capacity of power batteries in electrified vehicles (including HEVs, PHEVs, and BEVs) reached 504.4 GWh in the first half of 2025, a year-on-year increase of 37.3%. Asian companies continue to dominate the top 10 rankings, with the lineup unchanged: 6 Chinese firms, 3 South Korean firms, and 1 Japanese firm. However, SVOLT Energy replaced Sunwoda compared to the full-year 2024 list.

Chinese Firms Extend Lead, Korean & Japanese Players Decline

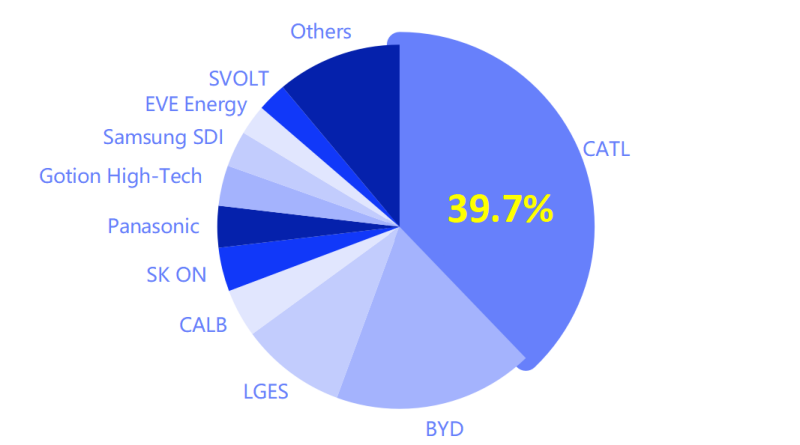

Chinese power battery makers collectively captured 68.9% of the global market share in H1, continuing their upward trend from 60.4% (2022), 63.5% (2023), and 67.1% (2024). Meanwhile, the combined share of the three major South Korean battery manufacturers (LG Energy Solution, SK On, Samsung SDI) fell to 16.4%, down 5.4 percentage points YoY. Samsung SDI was the only top 10 player to experience a YoY decline in installed capacity. Panasonic, primarily supplying Tesla, also grew slower than the industry average.

Domestic & International Gains Drive Chinese Expansion

SNE Research data shows consistent high growth in global power battery installations: from 59 GWh (2017) to 899 GWh (2024), with a CAGR of 47.5%. H1 2025’s 504.4 GWh represents a 37.3% increase over H1 2024 (367 GWh). Chinese firms were key drivers of this growth.

The six Chinese companies in the top 10 – CATL, BYD, CALB, Gotion High-tech, EVE Energy, SVOLT Energy – held a combined 68.9% share. Leaders CATL (37.9%) and BYD (17.8%) significantly outperformed peers. Including other Chinese firms outside the top 10, China’s global share exceeds 70%.

- CATL: Remained #1 with 190.9 GWh installed (+37.9% YoY). Supplies numerous Chinese automakers (Zeekr, AITO, Li Auto, Xiaomi) and global giants (Tesla, BMW, Mercedes-Benz, Volkswagen Group). Reported strong H1 results: revenue of ¥178.9B (+7.3% YoY), net profit of ¥30.5B (+33.3% YoY). Successfully listed on HKEX, establishing an “A+H” capital platform. Launched new products including 2nd-gen Shenxing Superfast Charging battery, Xaoyao dual-core battery, and sodium-ion batteries for passenger/commercial vehicles.

- BYD: Growth primarily fueled by internal demand as its EV sales surged 33% YoY to ~2.146 million units in H1. Its multi-brand strategy showed positive synergy.

- SVOLT Energy: Achieved the highest growth rate (+107.7% YoY) in the top 10, reaching 12.9 GWh. Key clients include Great Wall Motor, Geely, Stellantis, Leapmotor, and BMW MINI. Expansion in Europe (e.g., supplying Stellantis – 128k packs, BMW MINI – 110k packs, new smart brand contract) drove growth. Supplies LFP blade batteries domestically (Geely Galaxy E5, Ora Lightning Cat, Baidu Apollo RT6).

- Gotion High-tech: Second-fastest grower (+85.2% YoY) with 17.9 GWh installed, increasing share to 3.6%.

Domestic demand remains crucial: China’s H1 NEV production/sales reached 6.968M/6.937M units (+41.4%/+40.3% YoY), boosted by trade-in subsidies.

Weaker Demand Challenges Korean & Japanese Firms

Korean manufacturers’ declining share links to reliance on cooling European/North American EV markets and customers diversifying supply chains (often to Chinese firms) for cost/risk reduction.

- LG Energy Solution: 47.2 GWh (+4.4% YoY), share fell to 9.4% (from 12.3%). Hit by Tesla’s reduced orders (-28.9% YoY), partially offset by Kia EV3 success and GM EV sales growth in North America.

- SK On: 19.6 GWh (+10.7% YoY). Supported by Hyundai IONIQ 5, Kia EV6, VW ID.4/ID.7, but hampered by Ford F-150 Lightning slowdown (-13.4% YoY).

- Samsung SDI: 16.0 GWh (-8.0% YoY). BMW i-series sales dip (-5% YoY) and Rivian’s shift to Gotion’s LFP batteries impacted volumes, despite Audi Q6 e-tron growth (+8.8% YoY).

Combined Korean share: 16.4% (H1 2025) vs. 23.1% (2023), 18.4% (2024).

Panasonic: Ranked 6th with 18.8 GWh (+14.4% YoY), below average, share down to 3.7%. Heavily impacted by Tesla’s global sales decline (-13.3% YoY, especially in Europe). Slow EV transition by other Japanese clients (Toyota, Subaru, Mazda) offers limited near-term relief.

Global Expansion: Divergent Strategies

All major players are expanding overseas for growth, but with different focuses:

- Chinese Firms: Target Europe & Southeast Asia.

- CATL: Building plants in Hungary (operational late 2025, supplying Mercedes, BMW, VW), Spain (LFP JV with Stellantis, 50GWh by late 2026), and Indonesia (nickel/battery chain). Developing recycling.

- BYD, Gotion, EVE, SVOLT, Envision AESC, Sunwoda are accelerating overseas plants (Brazil, Hungary, Thailand, Germany, France, Spain, UK). SVOLT (Thailand), Gotion (Germany/Thailand), Envision (France) already operational. Transitioning from rapid expansion to “deep cultivation” via supply chain integration and localization.

- Korean Firms: Focus on Europe & North America. Established earlier in Europe, facing diversification pressure. Leveraged US IRA for JVs with GM, Ford, Stellantis (some operational). Adapting to US policy shifts (reduced IRA tax credits, FEOC rules) by boosting local capacity/raw material sourcing and reducing China reliance.

- Panasonic: Concentrated in North America & Japan. Also reducing China material dependence.

US Policy Impact: Uncertainty (e.g., expiring EV subsidies Sept 2025, FEOC rules) has led some to delay US projects (Panasonic, Envision AESC) or face risks (CATL-Ford JV).

Energy Storage Emerges as Second Growth Engine

With slowing EV growth, major battery firms are aggressively expanding into energy storage (ESS):

- SVOLT: Products in 30+ countries, 200+ projects. Secured >4GWh ESS orders in H1 (>50% export). Targets 5GWh (2025) and 8GWh (2026) ESS deliveries.

- CATL: ESS revenue reached ¥28.4B in H1 (-1.47% YoY but high base), contributing ~16% of total revenue. Gross margin rose to 25.52%. Launched 9MWh TENER Stack solution and mass-produced 587Ah ESS cell.

- EVE Energy: Using HK IPO funds for Hungary plant (30GWh, EVs) and Malaysia ESS project (38GWh, “multi-scenario global base”).

- Korean Firms: Targeting North America.

- LGES: First US ESS plant (Michigan, 16.5GWh) operational May 2025; targets 30GWh NA ESS capacity by 2026.

- Samsung SDI: Converting some EV lines to ESS production.

- SK On: Partnering with L&F for NA LFP supply to enter ESS market.

- Panasonic: Energy segment profit jumped 47% YoY (Q1 FY2025), driven by “better-than-expected” demand for data center ESS amid AI boom.