China’s Auto Market Consolidation: From Fragmentation to Concentration

The top 10 automakers in China have steadily increased their market share in recent years, yet concentration remains lower than in mature markets. Against a backdrop of slowing growth and intensifying competition, market consolidation and industry shakeout will dominate the sector for years to come.

The Shift to a “Survival-of-the-Fittest” Era

China’s auto industry has transitioned from rapid expansion to an era of stock competition. As BYD Chairman Wang Chuanfu predicted in 2022: “2023 will mark the start of the elimination race in China’s auto industry.” Over the past two years:

- Established brands vie for greater market dominance.

- Surviving newcomers fight to secure their foothold.

Rising Market Concentration (CRN)

Industry Concentration Rate (CRN) measures the combined market share of a market’s N largest players. As weak players exit and leaders consolidate:

- Markets shift from fragmented to concentrated.

- CRN rises accordingly.

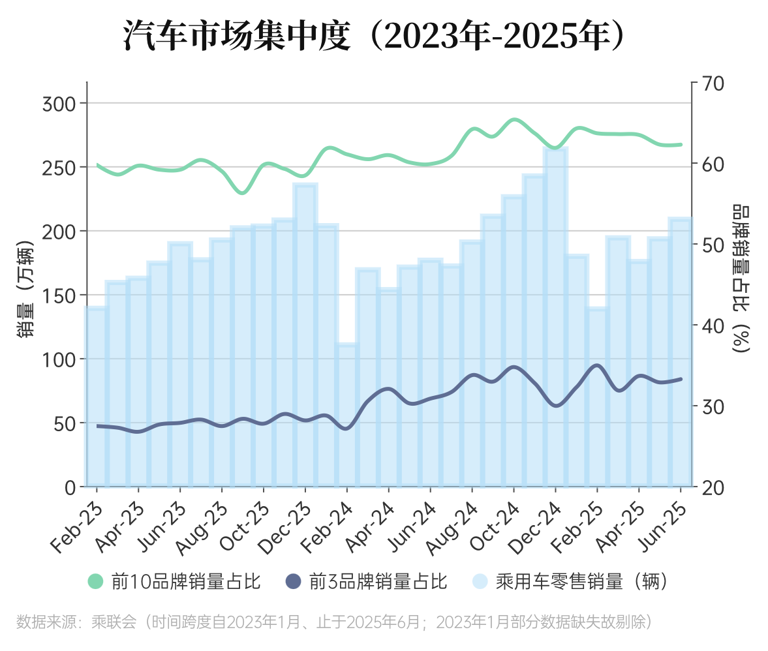

Data Spotlight: CR Trends (2023–2025)

Based on retail sales data from CPCA (China Passenger Car Association):

- CR10 (Top 10 players):

- 2023: 59% → 2025: ~65%

- CR3 (Top 3 players):

- 2023: 27% → 2025: 35%

This upward trajectory aligns with increasing competition in the new energy vehicle (NEV) era.

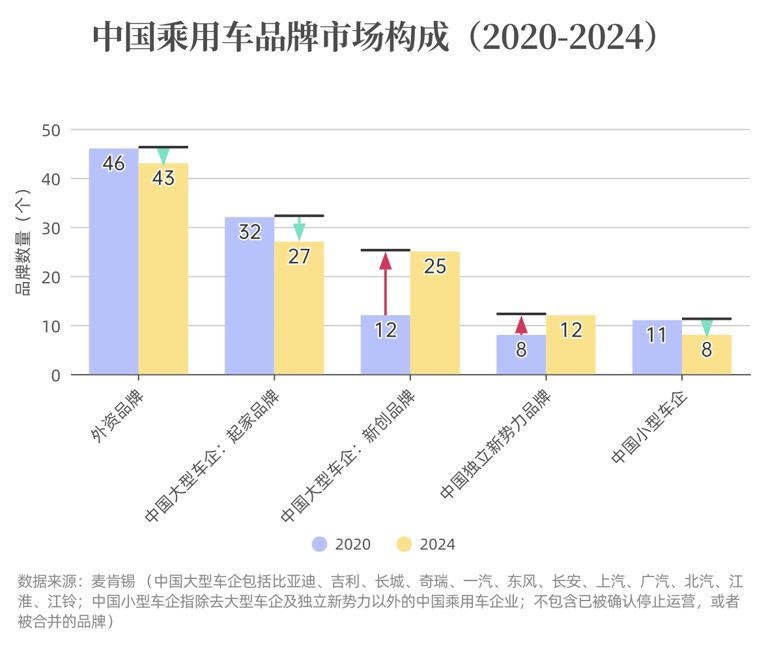

Market Reshuffle: Winners, Losers & New Entrants

McKinsey notes China’s auto “qualifying round” ended in 2019, followed by an elimination phase:

- Dominant brands (600k+ annual sales):

- 2020: 11 brands → 2024: 13 brands

- Mid-tier brands (240k–600k sales):

- 2020: 7 brands → 2024: 10 brands

- 9 are Chinese automakers; only 1 foreign

Key Shifts:

- Exits: Foreign brands retreated.

- New entrants: ⅔ of active EV brands are spin-offs from legacy automakers; only 12 are independent startups.

NEVs: Higher Concentration but Unstable Hierarchy

While NEV market concentration (CR3≈50%; CR10≈80%) exceeds the broader auto market, its competitive landscape remains volatile. Analysts attribute this to:

- Multi-brand strategies: Top players split sales across subsidiaries, diluting apparent concentration.

- Rapid small-brand growth: Gains and losses among smaller NEV makers offset consolidation.

NEV Leaderboard:

BYD dominates with 28.9% share—greater than the combined share of #2–#5 players. Its success stems from:

- Product diversity + aggressive pricing

- Mass-market brand recognition

Why Fragmentation Hurts: Goldman Sachs’ Warning

Despite consolidation, China’s market remains structurally fragmented:

- Top 10 players’ share: <80% (vs. >90% in developed markets).

- Active automakers: 49 (vs. ~30 in mature markets).

Risks of Fragmentation:

- ❌ Hinders industry-wide price coordination.

- ❌ Prevents efficient capacity adjustment.

- ⚠️ Widens cost gaps between top and lower-tier players → squeezes marginal players’ survival space.

The Consolidation Endgame: Oligopoly & Price Wars

As markets mature, a handful of giants typically emerge, wielding overwhelming scale, resources, and pricing power. During consolidation:

- Price wars erupt, often ignited by cost leaders.

- Wars end only when oligopolistic stability is achieved.

China’s Price War Truce?

After years of cutthroat discounts, regulators stepped in:

- Late June 2024: MIIT (Ministry of Industry and IT) and four ministries issued Guidelines on Regulating Auto Industry Competition, demanding:

- An end to “irrational promotions.”

- Price fluctuation monitoring.

- July 2024: BYD, Changan, BAIC BluePark canceled interest subsidies, retaining only state-backed “trade-in” incentives.

Outlook: Scale + Tech = Survival

Morgan Stanley forecasts:

- 2025 sales growth: 3% (to 28.3M units including exports).

- NEV penetration growth slows post-2026.

2025 is pivotal: Transition from volume growth to value restructuring.

- CR10 could reach 75% in 2–3 years (up from 65% in 2023).

- Ultimate survivors: Players with scale advantages + unassailable tech barriers.

The race isn’t just about speed—it’s about stamina and strategy.