German Luxury Trio Bets on Chinese Tech Partners in Bid to Halt China Sales Slide

BBA’s Shift in China’s Intelligent Driving Strategy: Embracing Local Solutions—Can It Reverse the Sales Decline?

The battle among Germany’s luxury auto trio—BMW, Mercedes-Benz, and Audi (BBA)—over next-gen Advanced Driver Assistance Systems (ADAS) in China has reached a resolution. Facing an increasingly fierce “arms race” in smart technology within China’s automotive market, all three have pivoted toward local suppliers, seeking solutions better tailored to local demands.

Localization Becomes Imperative

Recently, BMW Group announced a formal partnership with Chinese autonomous driving firm Momenta to co-develop a new intelligent driving system exclusively for the Chinese market. The solution supports full-scenario, point-to-point Navigation on Pilot (NOA), aiming to cover everything from parking to inter-city commutes (including automated parking), with a focus on China’s complex traffic conditions.

BMW’s decision effectively ends its earlier hardware-software collaboration with global chip giant Qualcomm in China. Similarly, Mercedes-Benz adjusted its strategy, abandoning its urban NOA partnership with NVIDIA in favor of working with Momenta (in which it holds a stake) to deploy localized features. Audi adopted a more flexible “multi-supplier” approach, partnering simultaneously with Huawei, Momenta, and CARIAD’s joint venture with Horizon Robotics (CoolRide).

Sales Crisis Amid “Off-the-Shelf Solutions”

BBA’s collective shift underscores the growing recognition of Chinese suppliers’ technological prowess and adaptability in intelligent driving. Adopting cutting-edge, China-savvy solutions has become essential for surviving this “red ocean” competition.

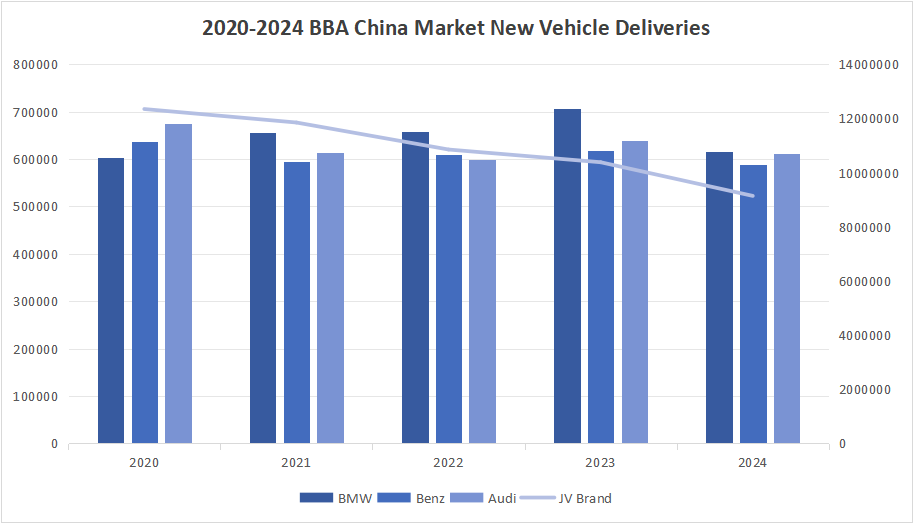

Yet, whether local partnerships can resolve BBA’s core challenges in China remains uncertain. Sales figures paint a stark picture:

- Mercedes-Benz: Q2 2024 sales in China plummeted 19% YoY to 140,400 units; H1 cumulative sales fell 14% to 293,200. Globally, Mercedes’ H1 sales dropped 8%, with its CEO recently expressing disappointment in China.

- BMW: H1 2024 China deliveries fell 15.5% YoY to 317,900 units—its steepest decline globally. A BMW executive candidly admitted, “The market is chaos. Today, BMW plays only a minor role in China.”

Behind the Sales Slump: A Multifaceted Crisis

- Structural Demand Shift: In 2024, premium car sales (¥300K+) in China fell 8.48%, with joint-venture brands down 18.45%. Electrification and smart features are eroding the “brand premium” of traditional fuel-powered luxury cars.

- “Price War” : To retain share, BBA joined discount battles. BMW’s repeated price cuts and protection U-turns in 2023 revealed strategic confusion. High-margin brands now struggle in a volume-driven market.

- Rise of Local Rivals: Brands like Huawei (Harmony Intelligence), Li Auto, and NIO are redefining “premium” with superior tech and faster iteration, aggressively capturing BBA’s market.

- Localization “Growing Pains”: Even with local partners, Sino-foreign collaborations face challenges in tech integration, quality control, and cultural alignment. Issues like lane-keeping inaccuracies and unstable NOA plagued Nissan’s Ariya N7 (using local smart cabin/driving solutions). Users also complained of laggy infotainment systems and poor app ecosystems.

- “Conservative vs. Aggressive” Clash: Traditional automakers prioritize functional safety and hardware reliability (e.g., strict EMC Level 5 standards), often lengthening development cycles. This contrasts with the “consumer electronics” approach of rapid iteration and post-launch fixes. Recent debates over non-automotive-grade 4nm chips (e.g., Qualcomm 8 Gen 3) in BYD and Xiaomi cars highlight this divide—Audi explicitly emphasized automotive-grade chips.

A Stopgap or Long-Term Cure?

Adopting Chinese solutions is a critical step for BBA to address urgent smart-feature gaps. BMW and Mercedes have already moved.

Yet this is far from a panacea:

- Shallow Collaboration: Current partnerships focus on localized adaptation of specific modules, not fundamental “Sinicization” of core platforms.

- Weak Internal Capabilities: Outsourcing key R&D risks ceding control over core tech and diluting competitive differentiation. Whether “fast-tracking” yields sustainable advantages is doubtful.

- Headquarters Hesitation: Global leadership remains cautious amid China’s upheaval. A Mercedes executive recently voiced unease over Europe’s reliance on U.S./Chinese AI and cloud services.

- Uncertain Global Export: No signs yet indicate BBA will deploy China-developed solutions worldwide.

- Holistic Competition: The real challenge isn’t just advanced ADAS—it’s a full transformation spanning electrification, smart tech, user experience, cost efficiency, and brand repositioning to rival the “all-round” strength of Huawei and Li Auto.

Conclusion

BBA’s embrace of Chinese intelligent driving solutions is a pragmatic response to fierce local competition. While it provides technical leverage to vie for smart-user-experience leadership, reversing sales declines and achieving brand renewal hinges on overcoming deeper structural challenges. The path forward requires evolving from “off-the-shelf” dependency to building endogenous competitiveness—fusing global vision with local insights while balancing safety, reliability, and innovation. The window for BBA’s adaptation in China is closing fast.