China’s EV Surge Redraws Global Auto Map Amid Growing Pains

Amid mountains of containers at Shanghai Port and the symphony of ship horns at Guangzhou Nansha Port, China’s auto exports have hit record highs.

The Numbers Tell the Story

January-April 2025: China exported 1.937 million vehicles, up 6% year-on-year.

EV Dominance: New energy vehicle (NEV) exports surged 52.6% to 642,000 units, accounting for 33.1% of total exports.

2024 Milestone: China exported 5.859 million vehicles globally last year, including over 2 million NEVs – equivalent to exporting the entire NEV fleet of the Netherlands onto the high seas.

This isn’t just growth; it’s a fundamental power shift. Since surpassing Germany in 2022, Chinese automakers have unleashed aggressive global strategies:

BYD’s “Global Car Sea Tactics” (rapid model rollout)

Great Wall’s “One Country, One Factory” localization

Geely’s “Acquire and Localize” approach

Rewriting the Rulebook (and the Rankings)

Defying the old narrative of “cheap and cheerful,” Chinese brands are now premium players:

Russia: 8 out of top 10 best-selling brands are Chinese.

Thailand: Chinese brands hold half the NEV top 10; BYD outsold Toyota at the Bangkok Auto Show.

Australia: BYD sold 3,207 units in April 2025 – 6x Tesla’s 500. Its Sealion 07 was Australia’s top-selling EV (734 vs. Model Y’s 280).

Europe: BYD outsold Tesla across 14 European countries in April 2025.

Gulf Region: Chinese market share projected to hit 15% in 2025 (up from 2% in 2019). Over 70% of Saudi and UAE buyers trust Chinese brands (MG, Geely, BYD, Changan).

“If we’ve learned one thing these past few years, it’s that China makes very good, affordable electric cars,” a UK analyst noted. “They’re not just knocking on the door anymore – they’re kicking it down.”

The Flip Side: Cracks Beneath the Surface

Despite the export crown (overtaking Japan for the second consecutive year in 2024), challenges loom large:

Market Concentration Risk:

Over 70% of export growth relies on “policy-friendly” markets (Russia, Mexico, Middle East).

Penetration remains below 5% in brand-critical markets: Europe & North America.

Policy Whiplash:

Russia: After filling the void left by Western sanctions, China faces new headwinds. Russia hiked import tariffs and recycling fees in 2025. Result: Jan-Feb 2025 exports to Russia fell 16% YoY (Chery, Geely down >30%).

Mexico: New rules mandate >40% KD assembly ratio to avoid US tariffs, forcing costly local production setup. The US’s 25% tariff on Mexican auto imports further complicates plans. Chinese automakers (Chery, JAC, BYD, Great Wall) have ~580k annual capacity in Mexico, with ~70% targeting the US market.

The “Value Trap” Persists:

Despite higher prices overseas, Chinese EVs still compete primarily on price:

BYD Dolphin in Thailand: Slashed from 699,900 THB to 559,900 THB (vs. Toyota Corolla Cross Hybrid at 999,000 THB).

MG/Geely prices in Gulf: 25-30% lower than equivalent Japanese/Korean models.

Consumer Perception: 72% of European buyers expect Chinese cars to be cheaper than established brands. A 27% price discount is typically needed to sway hesitant buyers (Escalent study). Concerns linger about after-sales support: “They’re running skeleton crews just to dump as many cars as possible,” remarked one European consumer.

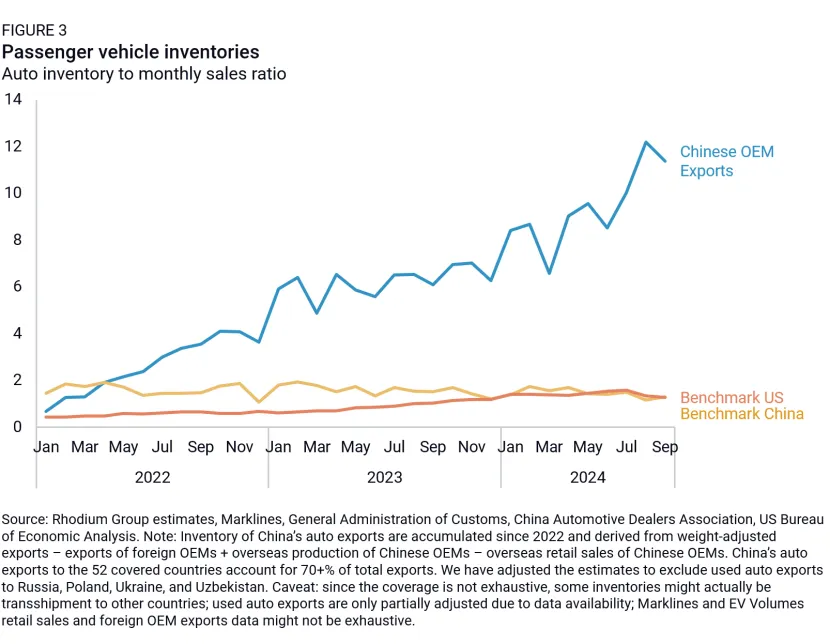

The Inventory Glut: Exports ≠ Sales

Rhodium Group (Jan 2025): Overseas sales significantly lag exports. Unsold inventory approaches 1 year globally – far exceeding US/China benchmarks.

Record Stockpiles: EU (28 months’ worth), Brazil (EVs: 22 months), Russia (16 months).

Dealer Collapse (Russia Q1 2025): 213 Chinese brand dealers closed – surpassing 2023’s total (187) and 3x Q1 2024. Besturn (-26 dealers), Kaiyi (-20), Dongfeng (-16) were hardest hit. Only 124 new showrooms opened (half of prior year).

Fire Sales: Russian dealers offered discounts up to 1 million rubles (vs. avg. new car price of 2.96M rubles) to clear stock.

The Road Ahead

Tens of thousands of Chinese EVs queue at Europe’s largest car transit port, Antwerp-Bruges, awaiting customs clearance. Their real battle – for sustainable market share, brand value, and profitability – is just beginning. While China has irrevocably altered the global auto landscape, navigating protectionism, inventory management, and the transition from “cheap” to “valued” will define the next chapter of its automotive ascent.